The Dubai Islamic Bank (DIB) has changed the way people in Pakistan get personal loans. DIB is known for following Islamic rules and putting the needs of its customers first. It provides a range of financial options that are in line with Sharia law. If you want to make smart financial choices in 2025, learning about DIB’s Personal Finance Loan can help.

Contents

- 0.1 What is a Personal Finance Loan?

- 0.2 Key Features of Dubai Islamic Bank Personal Finance Loan

- 0.3 How It Works

- 0.4 Fatwa

- 0.5 Features

- 0.6 Eligibility

- 0.7 Eligibility Criteria for Dubai Islamic Bank Personal Finance Loan

- 0.8 Who can apply for Personal Finance Facility?

- 0.9 In how many cities is this Facility Available?

- 0.10 Income Criteria

- 0.11 Finance Limit

- 0.12 Documents

- 0.13 How to Apply for Dubai Islamic Bank Personal Finance Loan

- 0.14 Benefits of Choosing Dubai Islamic Bank

- 0.15 Loan Limits and Repayment Plans

- 0.16 Challenges to Consider

- 0.17 Why Dubai Islamic Bank Stands Out

- 0.18 Common Uses of Personal Finance Loans

- 0.19 Tips for Managing Personal Finance Loans

- 0.20 Islamic vs. Conventional Loans

- 0.21 Future Trends in Islamic Financing

- 0.22 DIB Pakistan App in PlayStore

- 0.23 Conclusion

- 0.24 FAQs about Dubai Islamic Bank Personal Finance Loan

- 1 Shari’ah related FAQs

- 1.0.1 What are the needs that can be fulfilled from DIPF?

- 1.0.2 How does DIPF product work?

- 1.0.3 How does DIPF not inherit the element of Buy Back ?

- 1.0.4 What will be the mode of payment of installment?

- 1.0.5 What is the eligibility criteria for DIPF Facility?

- 1.0.6 Who can apply for DIBPF?

- 1.0.7 What are the documents required for DIPF Facility?

- 1.0.8 What are the likely dates for repayments?

- 2 Product related FAQs

- 2.0.1 Can co-applicant’s income be clubbed for the approval of financing limit?

- 2.0.2 How much time does the Bank take to approve the case?

- 2.0.3 What are the costs associated with availing the DIPF facility?

- 2.0.4 Is the processing fee refundable to the Customer in case his application is rejected?

- 2.0.5 What is the maximum limit of DIPF facility?

- 2.0.6 What is the minimum and maximum tenure for DIPF?

- 2.0.7 What is the eligibility criteria for DIPF Facility?

- 2.0.8 Who can apply for DIBPF?

- 2.0.9 What are documents required for DIPF facility?

- 2.0.10 What is EMP?

- 2.0.11 What if, the Customer doesn’t need financing facility after execution of the transaction?

- 2.0.12 What are the documents required for DIPF Facility?

- 2.0.13 What are the likely dates for repayment through Equal Monthly Payment (EMP)?

- 2.0.14 What is the maximum loan limit for Dubai Islamic Bank Personal Finance?

- 2.0.15 Is the loan process entirely Sharia-compliant?

- 2.0.16 What documents are required for application?

- 2.0.17 How long does the loan approval take?

- 2.0.18 Are there penalties for early repayment?

- 2.0.19 Related posts:

- 2.0.20 QarzMitra Loan App

- 2.0.21 JazzCash Islamic Saving Account 2025 (Salaam Investment)

- 2.0.22 Maryam Nawaz Loan Scheme: Youth Empowerment in Pakistan

What is a Personal Finance Loan?

Personal finance loans are basically a way for people to get money to pay for things like medical bills, school fees, or to combine multiple debts into one payment. The best thing about Dubai Islamic Bank’s personal loan is that it follows Islamic Sharia, which makes sure that all financial deals are honest.

Key Features of Dubai Islamic Bank Personal Finance Loan

The personal loan from Dubai Islamic Bank has a lot of features that make it stand out. What makes it special is this:

Islamic Sharia Compliance

DIB’s financing is in line with Islamic beliefs, so there is no Riba (interest) and all transactions are done in an honest way.

Flexible Payment Plans

The bank lets you choose a payback plan that fits your budget, which makes it easier to make monthly payments without going overboard.

Quick Processing

Everybody at DIB knows that time is money. You’ll get the money when you need it most because the application and acceptance process has been sped up.

Standard Chartered Bank Personal Loan in Pakistan

JS Bank Personal Loan in Pakistan

Faysal Bank Personal Loan Online

How It Works

- The Customer (with requirement of funds for personal needs) will approach the Bank to avail Personal Finance Facility.

- After the required credit approvals, the Bank will purchase specified goods (e.g. cotton, meat) from a commodity supplier on spot payment basis.

- The goods will be identified (i.e. the location and warehouse details) & disclosed to the bank by the broker.

- The Bank, after getting the title to and possession of the goods, will sell the goods to Customer on deferred payment basis.

- The possession (constructive) of goods will be given through a DO/DC in favor of Customer.

- The DO/DC issued will give absolute right to the beneficiary to possess the goods or to liquidate the same by selling it to the ultimate buyer.

- Special Sharia Controls have been added to ensure Sharia compliance of the product at various stages, so there’s no possibility /chance of returning goods to the original seller (directly or indirectly) and it will be strictly monitored on continuous basis.

Fatwa

Download Fatwa – English

PDF Download

Download Fatwa – Urdu

PDF Download

Features

- 100% Shari’a Compliant.

- Riba Free solution to your immediate cash needs like education, hospitalization, marriage etc.

- Avoiding Riba on your existing conventional loans through our product’s balance transfer facility.

- Lower rates for BTF customers.

- Financing limit from PKR 50,000 to PKR 4 Million (Terms & Conditions apply)

- Flexible tenor from 6 months to 48 months.

- Swift turnaround time and hassle free processing of your application.

- Affordable and competitive equal monthly installments.

Eligibility

Age Criteria

- Minimum Age = 23 years

- Maximum Age = 60 years>

Eligibility Criteria for Dubai Islamic Bank Personal Finance Loan

Before applying, it’s essential to know if you qualify. Here are the primary criteria:

Age Requirements

Applicants must be between 21 and 60 years of age at the time of loan maturity.

Employment Status

Both salaried professionals and self-employed individuals are eligible, provided they meet the bank’s income criteria.

Minimum Monthly Income

A steady income is very important. The necessary income requirement changes based on whether you work for someone else or for yourself.

Documentation Needed

Essential documents include:

- Valid CNIC

- Salary slips or proof of income

- Bank statements

- Proof of residence

Who can apply for Personal Finance Facility?

- Salaried Individual

How to Apply for a UBank Loan Online in Pakistan

UBL Personal Loan Apply Online in Pakistan

In how many cities is this Facility Available?

- Currently the product is being offered in Karachi, Lahore, Islamabad, Rawalpindi, Faisalabad along with following cities.

| Central Punjab | North | South | South Punjab |

| Gujranwala | Abbotabad | Hyderabad | Multan |

| Sialkot | Jehlum | Nawabshah | Sahiwal |

| Okara | Muzaffarabad | Mirpurkhas | Sargodha |

| Sheikhupura | Peshawar | Sukkur | Bahawalpur |

| Gujrat | Haripur | Quetta | Rahim Yar Khan |

| Kasur | Mirpur | Tando Allahyar | Burewala |

| Pattoki | Dadyal | Jhang | |

| Muridke | Chakwal | Toba Tek Singh | |

| Attock |

Income Criteria

- Salaried – Prime Customers : PKR 250,000 Gross / month

- Salaried – Known Company A & B Employees : PKR 30,000 Gross / month

- Salaried – Unknown Company Employees : PKR 35,000 Gross / month

- Salaried – Government Employees : PKR 30,000 Gross / month

- Salaried – Armed Forces Employees : PKR 30,000 Gross / month

- Salaried – Contractual (Known Company A & B Companies): PKR 40,000 Gross / month

Finance Limit

- Minimum Finance Amount – PKR 50,000

- Maximum Finance Amount – PKR 4,000,000

Documents

Documents required at the time of application:

- Dully filled Application form.

- Balance transfer undertaking ( In case customer wants to transfer his existing outstanding loan from another bank)

- Two recent passport size photographs.

- Copy of CNIC.

- All other relevant documents ( Income documents, Bank Statement, Profession proof etc. as per customer category)

How to Apply for Dubai Islamic Bank Personal Finance Loan

Getting started with your loan application is straightforward. Here’s a step-by-step guide:

Step-by-Step Application Process

- Visit the nearest DIB branch or their official website.

- Fill out the loan application form.

- Submit the required documents.

- Wait for verification and approval.

Online vs. In-branch Application

Online forms from DIB are easy to use and save you time and effort. But if you’d rather talk to someone in person, you can also go to a store.

Benefits of Choosing Dubai Islamic Bank

Opting for DIB’s personal finance loan comes with several advantages:

Sharia-Compliant Financing

Peace of mind knowing your finances align with Islamic principles.

Competitive Mark-Up Rates

DIB offers attractive rates compared to other Islamic banks, ensuring affordability.

No Hidden Charges

Transparency is a priority. All costs are disclosed upfront.

Flexible Tenure Options

Repayment periods range from 1 to 5 years, giving you the flexibility to choose what works best for you.

Loan Limits and Repayment Plans

DIB offers a range of loan amounts and flexible repayment terms to suit different financial needs.

Minimum and Maximum Loan Amounts

Loan amounts typically range from PKR 50,000 to PKR 2,000,000, depending on eligibility.

Available Tenure Periods

You can select repayment periods ranging from 12 to 60 months.

Early Repayment and Penalty Charges

The bank allows early repayment, but it’s essential to confirm any associated charges during the application process.

Challenges to Consider

While the loan has many benefits, it’s important to be aware of potential challenges:

Eligibility Barriers

Strict income and employment requirements might limit accessibility for some individuals.

Financial Planning Before Loan Application

Getting a loan means you have to pay it back. Making a budget and planning ahead are very important to avoid problems in the future.

Why Dubai Islamic Bank Stands Out

DIB isn’t just another bank; it’s a trusted partner in your financial journey.

History of Customer Trust

Since DIB has been doing Islamic banking for decades, it has built a reputation for being honest and reliable.

Diverse Financing Options

From personal loans to home financing, DIB offers a variety of solutions to cater to your needs.

Technological Advancements

DIB stays ahead of the curve when it comes to making things easy for its customers by offering services like mobile banking and online loan applications.

Common Uses of Personal Finance Loans

People use DIB’s personal finance loans for various purposes, including:

- Debt Consolidation: Simplify multiple debts into one manageable payment.

- Medical Emergencies: Cover unexpected healthcare costs.

- Education Financing: Support higher education or professional courses.

- Wedding and Event Expenses: Make life’s special moments stress-free.

Tips for Managing Personal Finance Loans

Taking a loan is only half the journey; managing it well is equally important.

Creating a Budget Plan

Outline your monthly expenses and set aside funds for loan repayment.

Avoiding Late Payments

Timely payments protect your credit score and avoid penalties.

Understanding Your Loan Agreement

Read the terms carefully to avoid surprises later.

Islamic vs. Conventional Loans

Key Differences

Islamic loans avoid Riba (interest), focusing instead on profit-sharing or service-based models.

Benefits of Choosing Islamic Financing

Sharia-compliant loans promote ethical and fair financial practices, aligning with personal and religious values.

Future Trends in Islamic Financing

The future of Islamic banking in Pakistan looks promising.

Growing Popularity in Pakistan

As awareness grows, more people are turning to Islamic financing.

Technological Integration in Loan Services

From customer service that is run by AI to digital loan forms, technology is making things easier to get and more accessible.

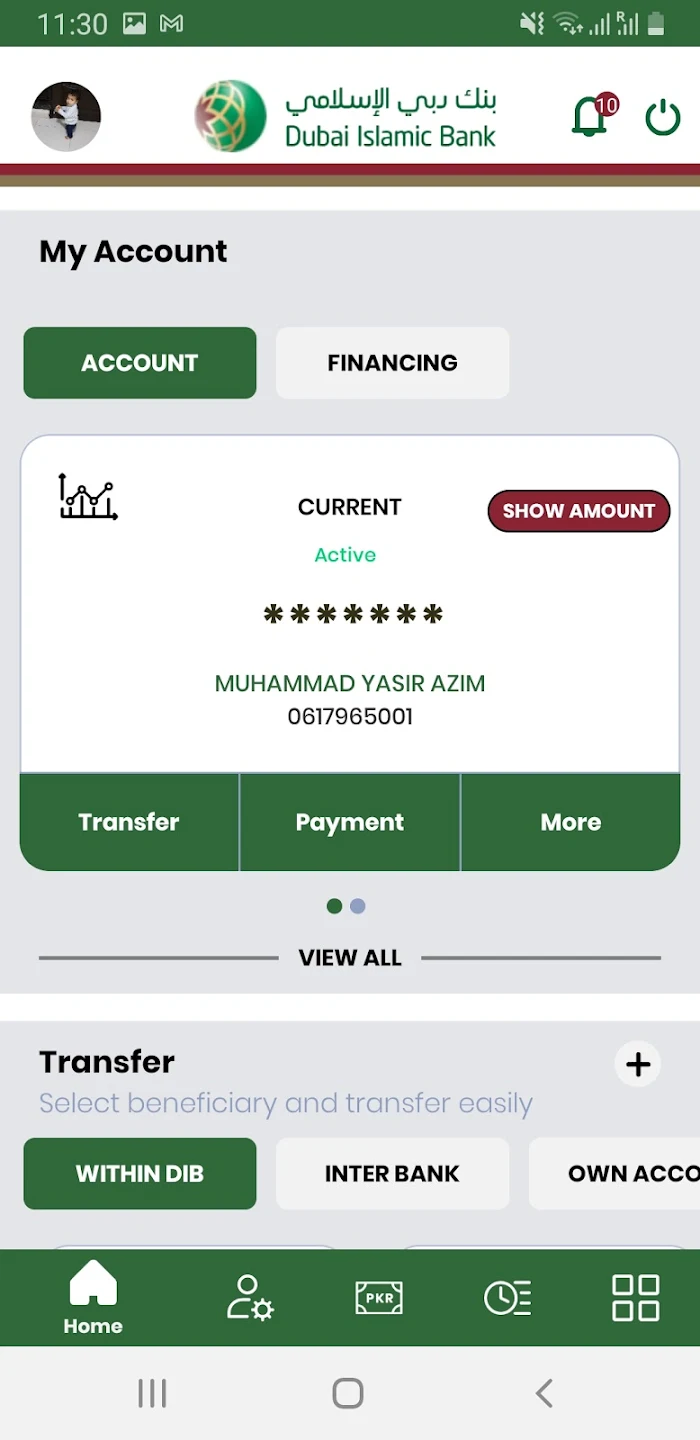

DIB Pakistan App in PlayStore

About this app

DIB Pakistan Mobile Banking App is designed to offer a full suite of banking services with a comprehensive range of features. The intuitive & user friendly interface provides a consolidated view of your relationship with the bank. You can also check your balances and make instant transfers / payments on the go.

Some key features of DIB Pakistan Mobile app include:

* Ease of login and usage of mobile app through biometrics

* Consolidated view of your relationship with the bank

* Setup recurring bill payments and transfers

* Instant fund transfer and bill payments

* All types of beneficiary addition via OTP.

* No additional PIN required for financial transactions.

* View all you historical activity and generate duplicate receipts.

* Viewing of Account Balances with mini or full statement download option

* Debit Card details with Mobile Top-ups and much more….

Conclusion

The Personal Finance Loan from Dubai Islamic Bank is a safe and Sharia-compliant way to get the money you need in 2025. DIB makes sure that solutions are fair, clear, and easy to use, whether you’re planning a big event or dealing with unexpected costs. Check out their services right now and make a smart financial choice.

FAQs about Dubai Islamic Bank Personal Finance Loan

What are the needs that can be fulfilled from DIPF?

DIPF facility is granted to Customers for meeting their immediate cash needs such as Education, Marriage, Medical Expenses or Settling of outstanding Conventional Loans in a Riba Free manner.

How does DIPF product work?

The Bank purchases specified goods (e.g. wheat, sugar, fabric etc.) from a supplier, directly or through an un-disclosed agent (Broker & Alliance Partner) on spot payment basis. After taking the title to and possession of the assets, the Bank sells the same to the Personal Finance Customer on deferred payment basis. The Customer after taking the constructive possession of the goods, may liquidate the same and fulfill personal need from these proceeds.

How does DIPF not inherit the element of Buy Back ?

A Buy Back transaction refers to the process of purchasing the commodity for a deferred price, and selling it for a lower spot price to the same party from whom the commodity was purchased. However, in Personal Finance, the goods are purchased from a commodity supplier first, then the same goods are sold to DIPF Customer(s) and the Customer liquidates these goods by selling it to the Broker/ Alliance partner.

What will be the mode of payment of installment?

The customer can deposit the installment amount in repayment account.

What is the eligibility criteria for DIPF Facility?

- Pakistani national and permanent resident of Pakistan.

- For Salaried Segment: Minimum 23 years and Maximum 60 years of age at the time of maturity.

- For Salaried segment: Minimum gross income of PKR. 37,000 (Net)

Who can apply for DIBPF?

- Existing DIB customers

- New to Bank salaried

What are the documents required for DIPF Facility?

a. Personal Information:

- Application form duly signed

- 2 recent Passport-size photographs of the applicant

- Copy of Applicant’s Current CNIC

- Relevant Income Documents (as per customer category)

B. Income Information Salaried Individuals:

- Original / Certified copy of Bank Statement showing Salary Credit

- Original / Certified copy of Pay Slip

- Employer’s certificate including Tenor /Designation /Salary

What are the likely dates for repayments?

The EMP date can be 3rd, 11th, 15th, 21st and 27th of the month depending on the date of disbursal.

Can co-applicant’s income be clubbed for the approval of financing limit?

Co-applicant’s income is not required to be clubbed for enhancement of the financing limit. Only applicant’s income will be considered for the approval of financing limit.

How much time does the Bank take to approve the case?

Generally cases are processed and approved within 2-3 weeks, subject to submission of complete documentation / information.

What are the costs associated with availing the DIPF facility?

The customer will need to pay Processing Fee:

- Up to PKR 5,000/-

The fee is charged subject to approval of facility. This fee will be inclusive of all legal documentations, verification and other charges etc.

Is the processing fee refundable to the Customer in case his application is rejected?

Processing fee is charged after the case is approved. Therefore if the application is rejected there is no need for refunding the same.

What is the maximum limit of DIPF facility?

We offer this facility ranging from PKR 50,000 to PKR 4,000,000. The facility amount and the tenure for individual cases are based on the sole discretion of the Bank.

What is the minimum and maximum tenure for DIPF?

The minimum tenure for DIPF is 6 months and the maximum tenure is 48 months. We offer this facility in the multiples of 6 months. You can choose a tenure ranging from 6, 12, 18, 24, 30, 36, 42 or 48 months).

What is the eligibility criteria for DIPF Facility?

- Pakistani national and permanent resident of Pakistan.

- For Salaried Segment: Minimum 23 years and Maximum 60 years of age at the time of maturity.

- For Salaried segment: Minimum gross income of PKR. 37,000 (Net)

Who can apply for DIBPF?

- Existing DIB customers

- New to Bank salaried

What are documents required for DIPF facility?

B. Personal Information:

- Application form duly signed

- 2 recent Passport-size photographs of the applicant

- Copy of Applicant’s Current CNIC

- Relevant documents (Income Documents etc.. as per customer category)

B. Income Information

Salaried Individuals:

- Original / Certified copy of Bank Statement showing Salary Credit for last 06 months OR

- Original / Certified copy of Pay Slip for last 03 months

- Employer’s certificate including Tenor /Designation /Salary

Business Individuals:

- Original / Certified copy of Bank Statement (last 12 months)

- 2 years Proof of Business (e.g. Tax return / Bank Certificate/ NTN Certificate / any other document)

C. Employment and Business Tenure:

Salaried

- Permanent job with minimum 2 year continuous working history in a same company.

- Direct company contract valid till maturity date of financing (Total 1 year previous working experience is mandatory). SEP & Business Individuals:

- Permanent job with minimum 1 year continuous working history in a same industry.

- Direct company contract valid till maturity date of financing (Total 1 year previous working experience is mandatory).

What is EMP?

EMP stands for Equal Monthly Payments. This Payment comprises both principal and Profit components. Please use the EMP Calculator to find out the EMP you need to repay.

What if, the Customer doesn’t need financing facility after execution of the transaction?

In case the Customer doesn’t want to avail the facility after execution of the Transaction, he will have to pay the processing fee to the Bank.

What are the documents required for DIPF Facility?

A. Personal Information:

- Application form duly signed

- 2 recent Passport-size photographs of the applicant

- Copy of Applicant’s Current CNIC

- Relevant Income Documents (as per customer category)

B. Income Information

Salaried Individuals:

- Original / Certified copy of Bank Statement showing Salary Credit

- Original / Certified copy of Pay Slip

- Employer’s certificate including Tenor /Designation /Salary

What are the likely dates for repayment through Equal Monthly Payment (EMP)?

The EMP date can be 3rd, 11th, 16th, 21st and 27th of the month depending on the date of disbursal.

What is the maximum loan limit for Dubai Islamic Bank Personal Finance?

The maximum loan limit is PKR 2,000,000, subject to eligibility.

Is the loan process entirely Sharia-compliant?

Yes, all financing by DIB adheres to Islamic Sharia principles.

What documents are required for application?

You will need your CNIC, proof of income, bank statements, and proof of residence.

How long does the loan approval take?

Loan approval typically takes 3-5 business days after submitting all required documents.

Are there penalties for early repayment?

DIB allows early repayment; however, it’s best to confirm the specific charges with the bank.

Say Job City in Pakistan for today latest jobs opportunities in private and Govt departments. View all new Government careers collected from daily. sayjobcity.com